Hi everyone!

I am so glad and thankful to have you all back today for a spring break special post. Looking back and reflecting on some previous posts, I’ve decided to revisit a few and dive deeper into the topics. With the first of these “throwback” episodes, I hope to jump back into “Credit: What Is It & How To Build It.” Last time, the main focus was on what exactly credit is, what goes into your score, and a general understanding of the history behind it. Today, I want to create a larger emphasis on the necessity to be careful with credit and what specifically does or does not go into affecting it.

Starting your Credit History

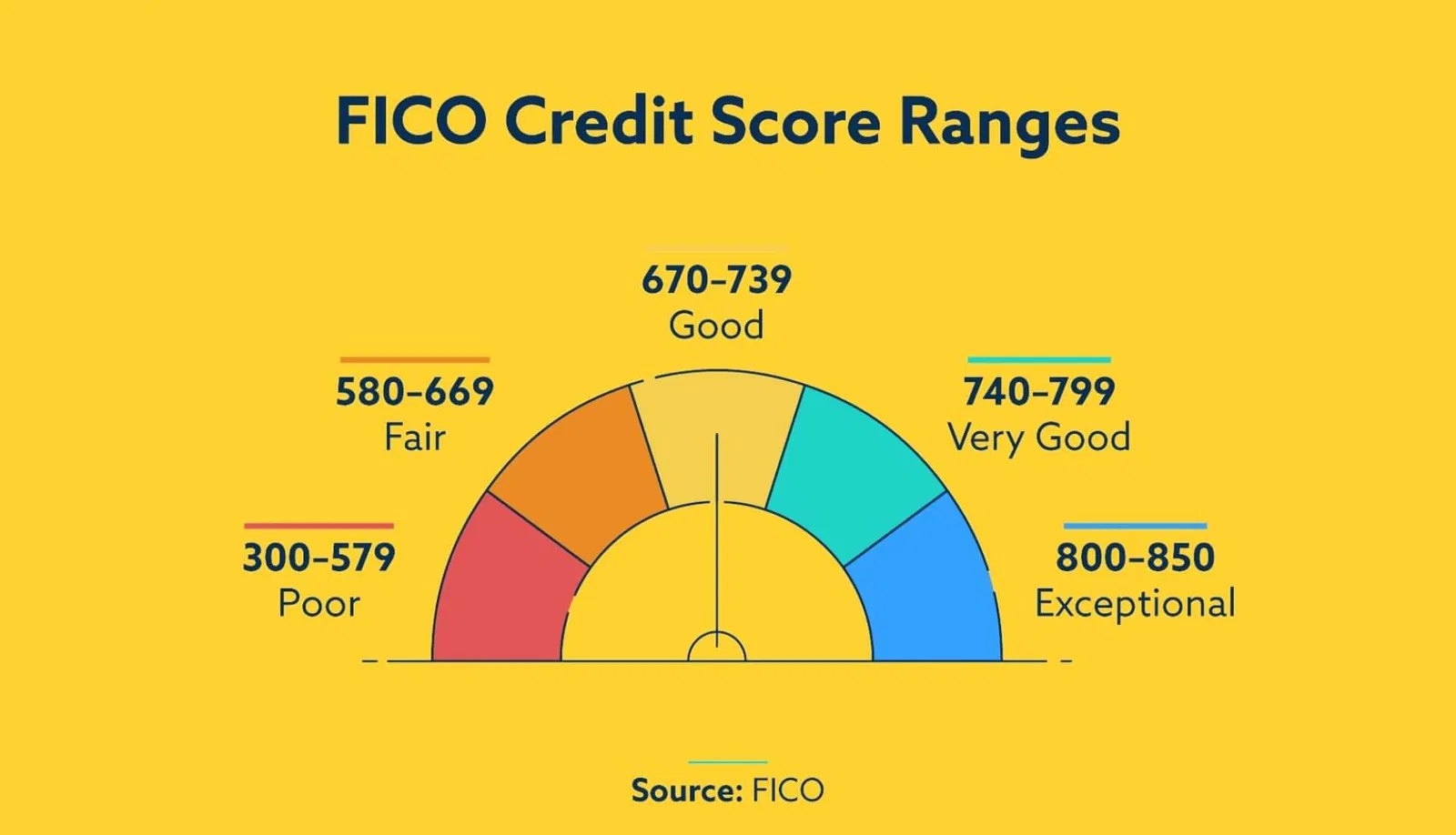

Arguably, the scariest part, getting started. When you first begin building your credit history, you may notice you start at the very bottom, a 300. This isn’t like a grade at school, where you start with an A and your grade lowers with bad scores. Instead, everyone starts at the bottom, and with time and making good decisions, you will likely see it rise. It’s important to note that most people begin building credit history with loans, for instance, student loans. It’s important to be aware of the repayment terms and for how long you’ll be paying that money back, as it can often range from 5 to 25 years. Your score may rise or fall for a variety of reasons, some seeming more backwards than others, however we will take that apart next!

The Straightforward and Twisty Paths To good Credit

As you may recall, your credit is basically your “trust score”, but to get to a point where you are seen as trustworthy can be far from straightforward. To begin, the most well-known way to raise your credit score is by paying off all your bills on time. If you consider yourself a forgetful person, look into setting up automatic payments with your bank. Another important part of building credit is not spending too much too quickly. When lenders see this behavior, it looks risky, and like you may not be a good contender for a larger limit. Generally, aim to spend from 10-30% of your limit, once again making sure to pay it back on time.

Why not overpay?

It may seem fairly simple. If you have some extra money, why not make a larger a larger payment and lower the amount you owe? In actuality this can often be harmful for your credit history, especially if it’s a low interest loan. Whats specifically being lost here is time. By paying the sum back quicker you have a shorter history with the bank and feel slightly less trustworthy to them. However it’s importnat to note that this drop is usually fairly minor, and if it may save you a large amount by not paying interest for as long of a period, its worth it.

Questions and Concerns

That all being said I hope the idea behind credit scores and their importnace becomes a little more clear to you! Feel free to leave a question, comment, or simply share something helpful in the section below. I would love to hear if you are enjoying these more in detail posts or want more of a focus on global issue like the last post.

Best,

GGF Team